Bank of America delivers steady growth amid margin pressures

Overview

Bank of America entered the second quarter of 2025 with stable earnings, supported by solid consumer activity, resilient asset quality, and consistent loan and deposit growth. Despite macroeconomic pressures and a slight sequential revenue decline in Global Banking segment, the bank maintained its trajectory of profitability and continued returning capital to shareholders.

Chairman and CEO Brian Moynihan emphasized the benefits of the firm’s disciplined strategy: “We delivered another solid quarter, with earnings per share up seven percent from last year. Net interest income grew for the fourth straight quarter, reflecting eight consecutive quarters of deposit growth and seven percent year-over-year loan growth. Consumers remained resilient, with healthy spending and asset quality, and commercial borrower utilization rates rose. In addition, we saw good momentum in our markets businesses. So far this year, we have supplied more capital to our businesses and returned 40 percent more capital to shareholders in the first half of this year than last year.”

Q2 2025 vs. Q2 2024:

- Net income was $7.1bn (+3% YoY), slightly up from Q1 due to lower pretax income, but still reflective of resilient core operations and improved consumer activity.

- Earnings per share rose to $0.89 (+7% YoY), continuing a four-quarter upward trend driven by disciplined cost control and stable revenue growth.

- Total revenue (net of interest expense) increased to $26.5bn (+4% YoY), aided by a 7% rise in net interest income (NII) and strong sales & trading performance.

- Consumer Banking revenue was $10.8bn (+6% YoY), supported by higher NII and strong digital engagement, with nearly 4.1bn digital logins and growing card spending.

- Consumer net income came in at $3.0bn (up from $2.6bn in Q2 2024), reflecting healthy spending levels and growth in investment assets to $540bn (+13% YoY).

- Global Wealth and Investment Management (GWIM) revenue rose to $5.9bn (+7% YoY), as client balances grew to $4.4tn and AUM flows remained strong.

- GWIM net income was $1.0bn, slightly down sequentially but in line YoY, with average loans increasing 7% YoY and strong digital engagement across Merrill and Private Bank.

- Global Banking revenue declined slightly to $5.7bn (-6% YoY), impacted by lower investment banking fees, while net income dropped to $1.7bn.

- Global Markets revenue was $5.3bn (+14% YoY), marking the 13th consecutive quarter of sales and trading growth, driven by equities (+10%) and FICC (+16%).

- Global Markets net income was $1.5bn, holding steady amid volatility, supported by improved performance in both trading and derivative segments.

- Consumer Banking revenue was $10.8bn (+6% YoY), supported by higher NII and strong digital engagement, with nearly 4.1bn digital logins and growing card spending.

- Net interest income reached $14.7bn (+7% YoY), driven by fixed-rate asset repricing, loan growth, and higher deposit balances across the consumer and wealth segments.

- Noninterest expense was $17.2bn (+5% YoY), up due to investments in personnel, brand, and technology, but down sequentially due to lower payroll tax expense.

- Provision for credit losses rose slightly to $1.6bn from $1.5bn in Q2 2024, consistent with stable charge-off levels and reserve builds in line with portfolio growth.

- ROE stood at 10.0% and ROTCE at 13.4%, both consistent with historical averages and reflective of a solid capital return framework.

- CET1 ratio was 11.5%, slightly down from Q1, but comfortably above regulatory minimums, highlighting the bank’s capital discipline.

- Book value per common share rose to $37.13 (+8% YoY), while tangible book value per share increased to $27.71 (+9% YoY).

- The bank returned $7.3bn to shareholders, including $5.3bn in share repurchases and $2.0bn in dividends, and announced an 8% increase in the quarterly dividend starting Q3.

Bank of America remains cautiously optimistic for the rest of 2025. While economic uncertainty and rate environment shifts may pose headwinds, strong deposit growth, stable asset quality, and continued investment in technology and talent are expected to support the bank’s long-term strategy.

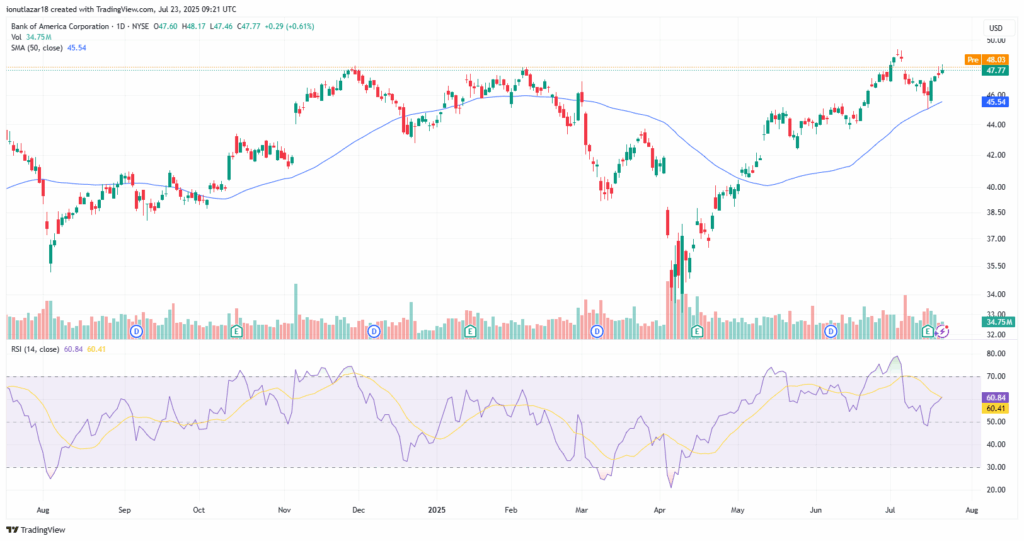

Following a minor dip after its Q2 2025 earnings release, Bank of America has shown resilience, rebounding above key technical support and closing. The stock continues to trade above its 50-day SMA, a positive signal that the broader uptrend remains intact. The RSI has recovered to 60.84, indicating a return of bullish momentum after briefly approaching neutral levels. Despite the short-term volatility, BAC has maintained higher lows and is now approaching resistance near the $48 level, last tested in early July. A decisive breakout above this area could open the path toward a retest of the $50 psychological level, while the $45-$46 zone remains key support in the near term.

Author: Andreea-Roxana Danci

Discover more from FSEGA Investment Club

Subscribe to get the latest posts sent to your email.