Mastercard’s global momentum continues in Q1 2025

Overview

Mastercard delivered strong Q1 2025 results, reflecting solid growth in consumer spending, cross-border travel activity, and strategic expansion in value-added services.

CEO Michael Miebach emphasized: “Our steady drumbeat of innovation continues. We launched Mastercard Agent Pay, our new Agentic Payments Program, and will work with companies like Microsoft and OpenAI. And we announced a strategic partnership with Corpay to deliver an enhanced suite of corporate cross-border payment solutions. While there is uncertainty in the world, we’ve built a diversified, resilient business model and proven strategy that enables us to effectively navigate various economic environments.”

Q1 2025 vs. Q1 2024:

- Net revenue grew to $7.3bn (+14% YoY and +17% currency-neutral), driven by strong performance across the core payment network and value-added services.

- Payment Network net revenue increased +13% YoY, driven by strong volume growth and renewed customer agreements.

- Total Gross Dollar Volume (GDV) reached $2.4tn (+9% YoY), with broad-based growth across geographies.

- Cross-Border Volume grew +15% YoY, driven by strong international travel trends and continued e-commerce momentum.

- Switched Transactions increased +9% YoY, a continued increase in transaction activity across digital and physical channels.

- Purchase Volume grew +10% YoY, reflecting robust consumer demand, especially in Europe and the U.S.

- Value-Added Services and Solutions net revenue increased +16% YoY, which includes 4 ppt from acquisitions, boosted by digital authentication, security, and engagement tools.

- Payment Network net revenue increased +13% YoY, driven by strong volume growth and renewed customer agreements.

- Operating income rose to $4.15bn (+15% YoY and +18% currency-neutral), supported by scale and pricing strength in high-growth areas.

- GAAP operating margin was 57.2% (+0.4 ppt YoY), while non-GAAP operating margin was 59.3% (+0.5 ppt YoY), reflecting disciplined cost control and mix shift to services.

- Total operating expenses increased to $3.1bn (+13% YoY), primarily due to higher general and administrative and advertising and marketing expenses.

- Net income recorded a value of $3.3bn (+9% YoY), while adjusted net income was $3.4bn (+10% YoY), a growth impacted by higher tax rates due to new global minimum tax rules.

- Diluted EPS was $3.59 (+11% YoY), while adjusted diluted EPS was $3.73 (+13% YoY), reflecting strong execution and capital returns.

- In Q1 2025, Mastercard returned approximately $3.2bn to shareholders, including $2.5bn through the repurchase of 4.7m shares and $694m in dividends.

- The company ended the quarter with $11.8bn remaining under its share repurchase authorization, reflecting its continued focus on disciplined capital returns and long-term shareholder value creation.

While Mastercard did not issue specific forward guidance, management reaffirmed confidence in the company’s ability to navigate macroeconomic uncertainty with its resilient, diversified business model. Strategic priorities include expanding value-added services, embedding AI into product offerings, and strengthening global partnerships. Management highlighted regulatory and tax-related headwinds (e.g. 15% global minimum tax impact) but expects continued momentum in volume, cross-border activity, and innovation-driven growth.

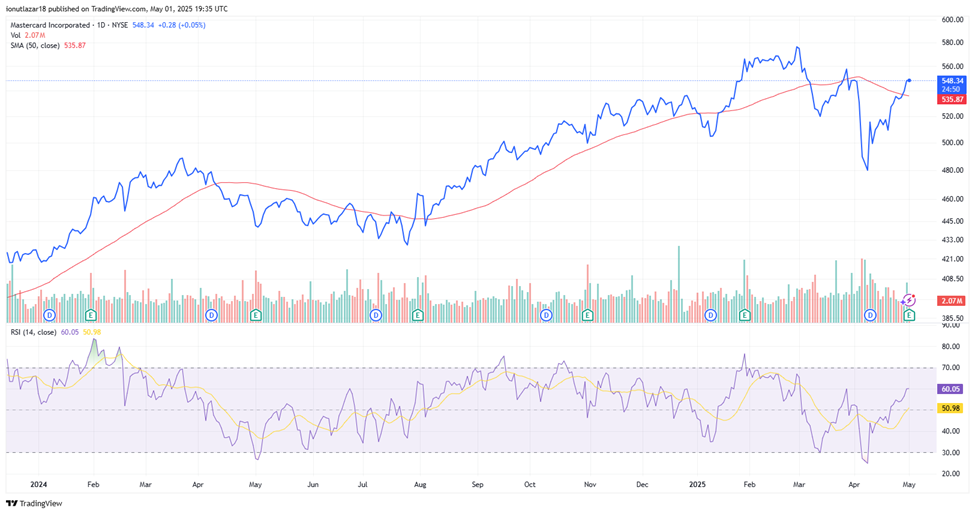

Although they managed to present solid financial results, which were above the estimates of Wall Street analysts, the lack of forecasts for the next period made investors quite skeptical, with the stock price of MA shares remaining relatively unchanged from the day before the quarterly report. However, at the beginning of this week, the share price managed to reach and even slightly exceed the value of the 50-day moving average, managing to appreciate in the first four months of this year by approximately +5%.

Author: Ionuț-Adrian Lazar